Dethrone: From Quantitative Easing to Digital Currencies - What's Next for the Dollar's Status Quo? (Part 2)

QE Unwind

Separating Fact from Fiction in the FED's Balance Sheet Reduction | July 2018

Many people have been discussing QE Unwind lately, often extrapolating beyond reality. It's important to understand that the details of the Federal Reserve's money printing are fully documented and verifiable on the FED's website. The FED's $4 trillion balance sheet was primarily used for two purposes:

- Purchasing Mortgage-Backed Securities (MBS) or subprime debt from US banks, totaling about $800 billion, to provide liquidity for lending to the real sector.

- Buying US Treasury Bonds, amounting to about $2.5 trillion, to suppress bond yields and provide funds for government economic stimulus and spending.

To reduce its balance sheet, the FED must sell these assets to receive dollars back, which it can then effectively erase those dollars out of thin air. This process mirrors the initial money creation.

It's true that QE money didn't fully reach the real sector. Banks that received QE funds for liquidity often:

- Bought US Treasury bonds for risk-free profits.

- Invested in various risk assets (stocks, commodities, currencies, gold).

Of the nearly $4 trillion in QE, a significant portion - close to $3 trillion - likely ended up in US Treasury bonds, rather than flowing into risk assets like the stock market as some have suggested.

While the FED is indeed withdrawing money, it's unlikely to recall all of it for two reasons:

- Most QE money is in US Treasury bonds. Unwinding QE means selling these bonds, which the FED may be reluctant to do as it holds about 20-25% of all US Treasury bonds, more than China and Japan combined. If the FED doesn't hold these bonds, who will, and at what price?

- Aggressively selling risk assets and causing a strong dollar inflow could strengthen the dollar to the point of damaging the US economy, which is likely the last thing the FED wants.

Looking at the FED's balance sheet over the past year, it has reduced by $180 billion, with $80 billion from Treasury bonds and $100 billion from other assets. The often-quoted figure of $2.5 trillion in potential withdrawals seems unrealistic and impossible without the FED dumping its own Treasury holdings.

For context, China holds $1 trillion in US Treasury bonds, and there are fears that if China were to sell these, it could potentially bankrupt the US government. It's therefore implausible that the FED would quickly sell its $2.38 trillion in bonds.

In conclusion, while the FED is indeed withdrawing money, the $2.5 trillion figure is likely exaggerated and causing undue concern among investors. During market downturns, it's crucial to be cautious about information that could negatively impact market sentiment. Always verify information before making investment decisions based on such news.

Entering a New Era of Interest Rate’s Hike

August 2018

The increasing bond yields in the US, Europe, and Japan might appear positive at first glance. They could suggest rising inflation rates and economic recovery. However, a deeper look reveals a hidden crisis of alarming proportions.

The real reason behind these rising interest rates is disconcerting: investors are abandoning government bonds. The situation could become even more precarious in the long term once central banks cease their bond-buying programs.

In the post-subprime crisis era, nations competed to lower interest rates to stimulate their economies and reduce public debt burdens. This strategy created a new problem: investors fleeing bonds in search of higher-yield assets.

As we transition into a post-quantitative easing (QE) world, we're likely to see a reversal. Major powers will increase interest rates in an attempt to attract capital back to their bond markets. This shift comes as central banks step back from their role as "white knights" swooping in to purchase bonds.

This new landscape brings back familiar concerns, chief among them the increased burden on public sectors. The question arises: how long will people continue to trust their governments?

Japan serves as a stark example. With the Bank of Japan (BOJ) holding 47% of government bonds, who will step in to purchase them if the BOJ stops?

The rising interest rates on Japanese bonds have been interpreted by some as reflecting higher inflation rates. This interpretation stems from the deeply ingrained mindset of "Homo Capitalus" - the belief that the state is the most trustworthy entity and that governments can never fail.

Some analysts remain optimistic, believing that even if central banks withdraw from bond markets, interest rates won't skyrocket. They argue that the private sector and various funds, still wary of the global economic situation, will continue to seek safe havens like the bond market.

However, this perspective may be too rooted in traditional economic frameworks, assuming that investment options are limited to bonds, stocks, and gold. In reality, new avenues for capital preservation are emerging and slowly gaining acceptance.

While some may scoff, I'm confident that certain cryptoassets will become recognized safe havens in the future. This shift will take time and only a select few cryptoassets are likely to pass muster as reliable stores of value.

If we can't answer who will hold government bonds moving forward, we're essentially playing a game of musical chairs. No one wants to be left standing when the music stops.

Consider the chart showing the sell-off of US bonds just before the government halted QE. It provides insight into why economic giants are now compelled to raise interest rates.

As we enter this post-QE era of rising interest rates, it's worth contemplating what forms of turbulence we might encounter. In my estimation, we won't have to wait long to find out.

Turkey's Economic Turmoil

A Crisis of Confidence and Its Global Implications | August 2018

The primary cause of Turkey's economic crisis isn't the strong dollar or American tax hikes. The problems have been accumulating since Erdogan took office. His administration has implemented several policies that have accelerated the erosion of confidence in Turkey's economy.

While it's often thought that governments can't fail as long as there's faith in the state, once that confidence disappears, it's game over. No matter how drastically you raise interest rates, if confidence is gone, it's merely treating the symptom, not the cause.

In my view, Turkey's current situation closely resembles Russia's crisis from a few years ago - a rapidly weakening currency and sharp interest rate hikes in a short period. However, a crucial difference lies in the details. During Russia's crisis, confidence in Putin's government remained strong, making the interest rate hikes an effective solution.

Turkey's crisis is the opposite - the public has lost faith in the government. In my opinion, the short-term solution involves seeking financial aid. More importantly, Erdogan's government needs to step down, allowing a new team to take over and swiftly implement policies to restore confidence. Forcing citizens to hold lira only breeds fear and exacerbates the situation.

Interestingly, one could potentially profit from arbitrage in such a scenario of severe currency depreciation and skyrocketing interest rates by going long on the lira and Turkish bonds. Eventually, both the currency and bond yields should converge to an equilibrium point (as happened with Russia). The caveat, of course, is that you must believe Turkey won't go bankrupt.

PS. On a related note, I've been questioning for years whether Europe has truly overcome its crisis. What has Europe done to solve its problems? The answer seems to be "nothing." Europe's issues persist and have even worsened, but they've been hidden behind the ECB's quantitative easing (QE) tool.

I've often suggested that if I had to guess, a bond crisis would likely start in Europe before the US or Japan. Of course, it would need a catalyst, and one can only hope that Turkey's crisis doesn't become that spark.

This situation underscores the fragility of economic systems based solely on confidence. It highlights the importance of sound economic policies and transparent governance in maintaining economic stability. As we watch Turkey's crisis unfold, it serves as a stark reminder of the interconnectedness of global economies and the potential for localized issues to have far-reaching consequences.

2024 Update

Despite Erdogan's government maintaining control of Turkey, it has failed to instill confidence in its leadership. The COVID-19 crisis of 2020-2022 further exacerbated Turkey's already struggling economy, pushing it into a more severe downturn.

As of 2024, Turkey's 10-year bond yield has surged past 26%, signaling a profound lack of creditor confidence. Even these high yields have failed to bolster faith in the lira, as people continue to abandon the currency en masse. This has led to a dramatic devaluation of the lira, edging the country closer to a state of hyperinflation.

The lira's depreciation has reached historic levels. In 2010, 1 USD exchanged for 1.52 TRY. By 2024, this rate had skyrocketed to 32.78 TRY per USD, representing a staggering depreciation of over 2,000%. If this trend continues, there's a high probability that the lira could collapse entirely.

In a classic sign of a failing currency, both real estate prices and the stock market in Turkey have soared to unprecedented heights. The Borsa Istanbul 100 Index has reached a new all-time high of 10,796 points. This simultaneous occurrence of severe currency depreciation and inflating asset prices is typical behavior in markets where the national currency is on the brink of collapse.

Adding to these worrying signs, many landlords in Turkey have begun conducting real estate transactions in US dollars instead of lira, further undermining the national currency.

Hong Kong's Real Estate Tightrope

Monetary Policy Constraints and Real Estate Bubble Concerns | August 2018

Hong Kong's monetary policy is inextricably linked to that of the US, as explained by Mundell's "Impossible Trinity" principle. This economic theory states that a country cannot simultaneously maintain:

- Free capital flow

- Fixed exchange rate

- Independent monetary policy

Hong Kong has chosen to maintain free capital flow and a fixed exchange rate (pegged to the US dollar), which necessitates forfeiting an independent monetary policy. This arrangement protects Hong Kong from currency crises like Thailand's Tom Yum Kung crisis, but it's not without its challenges.

One major impact is on Hong Kong's real estate sector. Looking at global property prices relative to income:

Hong Kong has the world's most expensive real estate (excluding Venezuela due to its failed state status). The Price to Income Ratio is 46.89, meaning it would take nearly 47 years of an average person's entire income to purchase a home. The yield on Hong Kong real estate is also extremely low at 1.89%.

For perspective, during my time in Hong Kong, I visited Repulse Bay, a popular beach and home to Hong Kong's ultra-wealthy. Some condos there were priced at HKD 150 million per unit (approximately 680 million baht).

In contrast, US real estate ranks 90th in affordability, with a Price to Income Ratio of 3.44 (still recovering from the subprime crisis). US property yields are around 2.9-3%.

From my perspective, Hong Kong's real estate appears significantly overvalued with low returns, especially as interest rates rise in tandem with the US. This disparity suggests that Hong Kong's property market may eventually need to correct, with people selling for profit and investing elsewhere. As prices adjust, yields should increase.

However, people have been predicting this bubble's burst for over a decade without it materializing. The current era is different due to the rising interest rate environment.

I'm not definitively predicting that Hong Kong's real estate bubble will burst - don't rush to short the market. Rather, I'm highlighting that such economic anomalies are becoming more common globally, with governments and central banks attempting to manage market mechanisms.

It will be interesting to observe how the world's most expensive real estate market fares in a rising interest rate environment.

2024 Update

As I explained in a previous article, the anticipated real estate crisis in Hong Kong didn't materialize in 2018-2019. Instead, what occurred was a significant uprising of Hong Kong citizens against their government.

The situation has since evolved dramatically. Following the onset of the COVID-19 pandemic and the Chinese real estate crisis in 2023, investors from mainland China began selling off their Hong Kong properties. As a result, residential property prices in Hong Kong have decreased by an average of more than 20%, with a continuing downward trend.

These developments have led many to reconsider Hong Kong's position as Asia's financial hub. The city's economic identity, once defined by its vibrant real estate market and status as a global financial center, is undergoing a significant transformation.

The Global Interest Rate Dilemma (Part 1)

Potential Consequences of BOJ and ECB Tapering Quantitative Easing | July 2018

The Bank of Japan (BOJ) and the European Central Bank (ECB) are reportedly planning to taper their Quantitative Easing (QE) programs in the coming months. This development raises questions about the potential impacts on bond markets, currency markets, stock markets, and the global economy.

Previously, concerns were raised about the US Federal Reserve's decision to halt QE and reduce its balance sheet, potentially draining liquidity from global capital markets. If similar actions are taken by Japan and the Eurozone, wouldn't this further reduce global liquidity?

To understand the implications, we must first examine the BOJ's use of QE.

The majority of the money printed by the BOJ has been used to purchase Japanese government bonds. In essence, the BOJ has been printing money to finance government spending. Currently, the BOJ holds an astounding 47.5% of all Japanese government bonds, equivalent to 433 trillion yen.

This figure has risen dramatically in recent years:

- 2016: 34%

- 2017: 41.6%

- 2018 (April): 47.5%

- (2024 Update) 2024, a new record in Japanese history, 53.34%

The BOJ's aggressive bond-buying was necessary because there was little appetite for Japanese government debt. As investors sold bonds, pushing yields higher, the BOJ stepped in to buy bonds at any price to keep interest rates low.

If the BOJ were to end QE, who would buy these bonds? And what would happen to the bond market when current bondholders realize there's no longer a guaranteed buyer at any price?

A sudden halt to QE could lead to a rapid outflow of money from the bond market, causing interest rates to spike. This raises the question: where would this money go?

One possibility is the Japanese stock market. Previously, Japan's Government Pension Investment Fund (GPIF) sold government bonds and invested in stocks, briefly driving up the Nikkei index. If this pattern repeats, it could strengthen the yen as foreign capital flows into Japanese equities.

However, if the money flows to other markets, the yen could significantly weaken. If investors still prefer low-risk bonds, they might turn to US Treasuries, which offer better yields and are perceived as less risky. This scenario could contribute to continued dollar strength.

Long-term, if the Japanese government struggles to borrow and faces high interest rates, the Japanese economy could be approaching an "end game" scenario.

The situation with the ECB is similar, and potentially even more severe.

The Global Interest Rate Dilemma (Part 2)

Why the Euro is Trapped and the Dollar May Strengthen | August 2018

One of the most significant conflicts in the current global economic structure is the discrepancy in interest rates across different economies. This situation creates a complex dilemma for major economic players.

It's unfeasible for the United States to raise interest rates in isolation. Such a move would trigger a massive influx of capital into the US, particularly if other countries maintain near-zero interest rates. However, it's equally improbable for the Eurozone or Japan to increase their interest rates. Doing so could potentially destabilize their bond markets and substantially increase government debt burdens, undermining their creditworthiness.

The European Central Bank (ECB) faces a particularly challenging situation. If it continues quantitative easing (QE) and maintains low interest rates (as Italy has been advocating), it might temporarily support the bond market. However, this approach would likely result in capital outflows as investors seek higher yields elsewhere, primarily in US dollars and Treasury bonds.

Conversely, if the ECB were to halt QE and raise interest rates, it could lead to a collapse in the bond market due to lack of buyers. Paradoxically, this scenario would also likely result in capital flight as investors move away from perceived high-risk assets towards safer options - again, primarily US dollar-denominated assets.

This analysis leads to a personal observation: the Euro appears to be in a no-win situation, while the US dollar seems poised for further strengthening regardless of which scenario unfolds.

PS. It's worth noting that there might be an extremely challenging - and likely belated - option for the Eurozone. This would involve consolidating all debt within the Eurozone into a single debt market and accepting a substantial write-down of debt for the weaker economies within the bloc. However, the political and economic hurdles to implementing such a solution are formidable.

Global Economic Crossroads

Interest Rates, Stock Markets, and Currency Dynamics in the Post-Low Interest Era | October 2018

Global stock markets have experienced significant corrections due to concerns over rising US interest rates, which have now surpassed 3%. According to economic theory, when interest rates increase, money tends to flow back into low-risk debt markets such as government bonds, corporate bonds, or bank deposits. Additionally, higher borrowing costs typically lead to slower business expansion, cooling both the economy and the stock market.

The problem arises from the fact that the world has been in a low-interest rate environment for nearly a decade. Suddenly, the United States has begun raising rates continuously, citing economic recovery (whether this recovery is genuine is a separate discussion).

This situation has led to several ongoing issues following the US interest rate hikes:

- Investors, concerned about rising interest rates, have been selling stocks, causing the Dow Jones to drop significantly in recent periods.

- The interest rate disparity between the US and other countries is widening progressively.

- Other countries, such as Thailand, face two choices: either raise interest rates to follow the US or maintain current rates.

- If Thailand chooses to raise rates, the economy may slow down as theorized. Given that our economy is still in a precarious state, this could potentially lead to a severe recession.

- However, if Thailand opts to maintain current interest rates, the widening gap between Thai and US rates may risk capital outflow to the US to capture higher interest rate differentials or engage in carry trades (borrowing in low-interest countries and lending in high-interest countries).

- Imagine a scenario where almost every country in the world cannot adjust their interest rates to match the US quickly enough. Inevitably, some capital will flow back into the United States, likely resulting in continuous strengthening of the dollar.

- Some of the money flowing into the US may not just park in the bond market but could cycle back into the stock market. The trend of a strengthening dollar might contribute to continued growth in US stocks (similar to when Japan faced the Plaza Accord, causing rapid yen appreciation).

- This point contradicts the economic theory stating that rising interest rates cool down the stock market. This discrepancy arises because, historically, stock markets were driven by a country's economic fundamentals, whereas currently and in the future, stock markets are driven by capital flows in and out of countries.

- However, the problem doesn't end there. A long-term strengthening dollar is not beneficial for the United States or US businesses. This implies that in the future, we may see a situation where fundamental factors are not conducive to business growth (high interest rates, strong dollar), yet the stock market continues to advance due to capital inflows.

- Meanwhile, other countries, especially those in emerging markets, will face capital outflow crises, leading to currency depreciation. When currencies weaken, economic crises may follow, particularly due to increased foreign currency debt burdens.

We may need to prepare ourselves for the possibility that in 2019 and beyond, the global economy could stagnate or even face economic crises in strange, unprecedented forms that we've never encountered before.

US Interest Rate Hikes, Trade Wars, and Worldwide Stock Market Declines

October 2018

I want to emphasize that this article reflects my personal viewpoint. Please read it critically and use your own judgment.

There's a hypothesis I've held for a long time: the reason behind the US raising interest rates isn't due to economic recovery as they claim, but rather a step in a global financial game. The US, as a major player, is expertly maneuvering to control the trajectory of global finance according to their own design.

- The concern initially stemmed from worries that the massive printing of US dollars (the FED's balance sheet grew from $0.8 trillion pre-QE to about $4.2 trillion post-QE, a 500% increase) would lead to dollar devaluation. This didn't actually happen because much of the newly printed money flowed into debt markets (QE -> buying government bonds) and capital markets (QE -> buying banks' subprime assets -> banks investing this money in capital markets and bond markets for profit). However, it didn't reach the real sector, meaning actual businesses didn't benefit from this QE (the beneficiaries were the government, which got free money to spend liberally, and big banks, which got extremely low-cost capital to make money).

- Other major economies followed the US in implementing QE, including the Eurozone, UK, and Japan. This led to a global flood of money, causing the value of almost all asset types to skyrocket over the past decade.

- But the hidden problem for all these powerful governments is that their central banks are increasingly becoming their creditors. Central banks are printing money to buy government bonds (or simply put, printing money for the government to borrow and spend).

- Central banks can't print money indefinitely because eventually, it would destroy the state's creditworthiness. So, at some point, money printing must be stopped. But the problem that follows is even bigger: if central banks stop printing money, who will buy the bonds (who will lend money to the government)?

- The FED held about 20% of US government bonds at that time. The ECB held about 40% of Eurozone bonds. The BOJ was the most extreme, holding about 47% of Japanese government bonds. In simple terms, central banks had become creditors for nearly half of their governments' debt.

- If all countries truly stopped QE and absorb all this money from the economic system, no one would be interested in lending to governments anymore. The world powers would collapse from a bond crisis. This is inevitable, sooner or later, because no one can print money forever.

- This is where the crucial mechanism of the US comes in. If the FED stops QE and withdraws money, the key to preventing US collapse is "creating incentives for people to be interested in holding bonds instead of the FED." How do you make people want to lend money to the US?

- The method is to "raise interest rates." Although continuously raising interest rates over a long period would cause investors to lose on face value (Mark to Market), the yield on US bonds would still be higher than the yield on other nations' bonds.

- The FED thus seized the opportunity to reduce QE starting from late 2016 (by now, they've withdrawn about 10% of the money they printed, or approximately $0.5 trillion from the system) and raised interest rates to attract money flow into US bonds, which now offer yields above 3% while global bond yields remain low, with some even negative.

- With each round of the FED rolling out new bonds, we notice the dollar strengthening significantly. This mechanism of drawing money back to the US is a long-term process (unlike during the subprime crisis, which was a sudden withdrawal). This means money from QE that had flowed into global capital and debt markets over the past decade is now flowing back to the US due to interest rate differentials.

- To accelerate this movement and make it more intense, trade wars are being used as a tool to create uncertainty in the global economic system. (In "Risk On" mode, money flows from low-yield to high-yield assets, but in "Risk Off" mode, when people fear economic crisis, money flows from high-risk to low-risk assets). As fear of trade wars grows, money is likely to flow from stock markets back to bond markets, which are perceived as lower risk.

- And which bond market do people believe is low-risk while offering higher returns than others? It's none other than the US bond market. This explains why stock markets worldwide are being sold off, with continuous outflows, leaving many people puzzled as to why foreign investors seem to be selling relentlessly throughout the year.

- So who stands to lose? Right now, major powers like the Eurozone and Japan are in a tight spot. Their economies haven't fully recovered, yet they face interest rate differentials due to US rate hikes. They have limited options: (a) stop printing money and raise interest rates to follow the US, or (b) maintain current rates and, if money keeps flowing out, keep printing money to buy bonds.

- Option (a) is extremely difficult because the Japanese and Eurozone economies are still fragile. Raising interest rates could catalyze an economic crisis. Option (b) is dangerous because prolonged money printing will erode state credibility and eventually lead to an end game.

- This game is like musical chairs - whoever sits first has the advantage. The US has now taken the first seat, and everything is going according to plan. The dollar is strengthening, money is flowing back into the bond market, while the Eurozone and Japan are in a concerning position, especially if the interest rate gap continues to widen.

- Certainly, the central banks of both the Eurozone and Japan have limited weapons left. If central banks continue to hold more government bonds, it will accelerate the erosion of state credibility. But to stop printing money and incentivize people to hold bonds, the only way is to raise interest rates. Whichever path they choose, enormous risks await in the next few years.

- If my thoughts are somewhat close to reality, what we'll see next is deflation due to dollar appreciation, as well as continued stagnation in global stock markets due to the mechanisms mentioned above.

- But the economic game doesn't have just one player like the US I believe that after this, other countries will develop mechanisms to counter this game. Whether they succeed or fail, we'll have to keep watching. But it seems the Eurozone and Japan are truly in a difficult situation.

AI, Automation, and the Future of Work

From Economic Pain to Utopian Possibilities | November 2018

After reading the first chapter of Kai Fu Lee's "AI Superpowers," I find that his perspective confirms my beliefs about the long-term displacement of human jobs, which will align with declining birth rates. In the next 10-15 years, we're likely to see significant pain in the global economic system due to the combination of an aging society and A.I. disrupting the human workforce. A crisis in social security systems seems almost unavoidable.

However, as our children's generation grows up, this crisis could transform into an opportunity. In about 30-40 years from now, there will be fewer children, coinciding with the increased presence of AI replacing human workers. The world may enter a new era where there's no longer a working class (of humans).

In a world without a human working class, I personally think:

Marxism might become more interesting than capitalism.

The failure of Marxism stemmed from the inability to fully harness the potential of the proletariat. But when robots become the workers, this problem should disappear because we'll no longer have a human proletariat.

Expanding the size of government might be better than reducing it.

Currently, I agree with downsizing the public sector and allowing the private sector to take over, due to the inefficiency of government being a drag on national progress. But imagine a government without human bureaucrats. I believe expanding such a government would lower the cost of the welfare state and could make Universal Basic Income (UBI) a reality.

I see the future world as more of a Utopia than a Dystopia. However, before we reach that point, the global economy will have to endure a painfully difficult transition period.

China and Techno-utilitarian Approach

A Keynesian Gamble on AI Supremacy | December 2018

Kai-Fu Lee's "AI Superpowers" highlights China's "Techno-utilitarian approach," where the state actively participates in driving technological advancement. This involves providing funding, infrastructure, tax policies, legal adaptations, and other support to researchers and AI startups, enabling them to develop AI technologies at lower costs and with greater convenience.

This approach has propelled China ahead in AI research, potentially overtaking the US in the near future. China's advantage lies in its vast amount of data from O2O (Online-to-Offline) services, unparalleled by any other country.

From an economic perspective, this Techno-utilitarian approach can be seen as a form of Keynesian’s state intervention. The government stimulates the economy by investing heavily in AI. Inevitably, this leads to increased public debt (and certainly involves wastage from failed projects).

Many countries criticize China for this, given the alarming debt figures and instances of failed state interventions in industries like solar panels and steel. However, the Chinese government is willing to bet on AI because if successful, it could trigger a major economic shift, catapulting China's economy forward dramatically.

For instance, China has built Xiongan, a city designed with roads for autonomous vehicles, serving as a massive lab for self-driving car experiments. This contrasts sharply with the US, where trucking unions still oppose self-driving car research.

This approach addresses the issue of institutional lag discussed in Alvin Toffler's "Revolutionary Wealth," where slow-changing institutions, especially legal ones, hinder human evolution. China is tackling this problem head-on, potentially allowing it to leapfrog the US in just a few years.

If successful, this could transform China into a global economic leader, improving areas like accident reduction, logistics efficiency, and productivity. However, it's crucial to remember that this economic shift will also have far-reaching impacts on traditional automotive industries. This transformation isn't limited to China; it will have global repercussions, including significant effects on countries like Thailand, which is a major automotive parts manufacturer.

The challenge lies in balancing this transformation with support for affected industries and citizens, potentially through reskill training programs or Universal Basic Income (UBI).

This approach aligns with Keynesian economics: state intervention to improve business efficiency and effectiveness. Initially, it leads to deficit spending and increased public debt. However, when the economic shift occurs, investments begin to pay off, domestic businesses become more competitive, costs decrease, and the state ultimately benefits from increased tax revenues to offset initial investments.

This is "Good Keynesian" economics, which China is attempting. It's a two-birds-with-one-stone strategy:

- Stimulating the economy as growth slows down

- Creating an economic shift to accelerate China's path to global AI leadership

Currently, China's Techno-utilitarian approach and vast O2O data are the two main factors pushing China ahead in AI, leaving other nations increasingly behind.

Real Estate Appreciation

A Limited Resource? | December 2018

Many believe that holding real estate is a long-term wealth preservation strategy, rooted in the traditional notion that property values invariably increase over time. However, as global demographics shift towards an aging population, we must reconsider this assumption.

With declining birth rates and shrinking populations, what does the future hold for real estate prices? As demand decreases, the average price of supply is likely to follow suit in the long run. This doesn't mean all property values will uniformly decline; rather, we can expect increased variance in the market.

This variance implies that properties in less desirable locations may experience significant price drops, while prime locations maintain their high values. The price gap between different areas will widen, making real estate investment an increasingly complex endeavor.

Japan serves as a prime example of this trend. The country is already witnessing a phenomenon where numerous houses are being offered for free, as owners struggle to keep up with taxes and maintenance costs. Yet, in prime locations like Shibuya, Ginza and Namba, property prices remain consistently high.

As one of the first nations to fully enter an aging society, Japan now has 40% of its population at retirement age. The next decade will see Japan's population decline at an accelerated rate. This demographic shift will have far-reaching effects on the economic system in the coming decades.

Thailand is also transitioning into an aging society. This demographic change will likely constrain domestic consumption growth, and the real estate market may follow a trajectory similar to Japan's.

While this problem seems insurmountable, there is potential for Thailand to revolutionize its economic system. However, this would require bold leadership and visionary governance - a combination that remains uncertain in the current political landscape.

The Game the State Can Never Win

Europe's Economic Dilemma | December 2018

The recent Yellow Vest protests in France, while seemingly about fuel tax hikes, actually reflect a deeper, more complex economic crisis facing not just France, but the entire European Union. This crisis is the culmination of years of unnatural economic policies that have left European nations in a precarious position.

At the heart of the issue is a series of interconnected problems:

- European states have been providing welfare benefits beyond their means, running budget deficits to stimulate their economies. This has led to steadily increasing national debts. Unlike during Thailand's Tom Yum Kung crisis, Eurozone countries can't use monetary policy to stimulate their economies due to the shared currency.

- With mounting debts, states struggle to borrow. The European Central Bank (ECB) has resorted to printing money, becoming a major creditor (owning about 40% of total European debt).

- To manage debt burdens, interest rates have been pushed to near-zero or negative levels. However, this hasn't stopped debt from growing. The question remains: how can quantitative easing (QE) be stopped when no one else wants to lend to Europe?

- Governments are caught between needing to increase revenue and reduce spending. However, stimulating the economy through tax cuts reduces revenue - the opposite of what's needed.

- With reduced income, states must implement austerity measures and find ways to increase tax revenue. The fuel tax in France is just the first manifestation of this problem. Future measures may involve various forms of extracting money from citizens.

- This game is merely a way for states to drag their feet, as it's a path they can never win. Stimulating the economy by cutting taxes reduces revenue, forcing governments to find other income sources. Without fiscal policy to stimulate the economy, there are no other tools available, as monetary policy is not an option within the Eurozone.

- Aggressive fiscal policies lead to mounting debt that can't be sustained even with money printing. The Eurozone's credit rating still lags behind the US, which has already begun reducing QE and raising interest rates.

- Eventually, tax hikes may lead to a crisis of faith, resulting in social unrest. This could be the trigger that erodes trust in the state.

- Once trust is lost, the long-simmering government debt crisis may explode. People lose faith in the state (the debtor), money flows to lower-risk options, Eurozone interest rates spike, leading to a Sovereign Debt Crisis. Funds may flood into the US, perceived as safer and offering higher interest rates.

- What began as small protests could be rooted in long-standing issues that governments have been kicking down the road. If not addressed promptly, this problem could trigger a chain reaction leading to issues far greater than we can imagine.

I've previously suggested that if a new economic crisis were to occur, Europe would be a likely epicenter. Since the ECB began printing money, there's been no fundamental improvement in Europe's economic situation.

Let's hope I'm wrong, and that Europe can resolve these issues soon.

Will the US Collapse? (Again?)

January 2019

For a decade, there's been talk about high US debt, potential bankruptcy, and the dollar's devaluation. Let's examine this objectively, based on facts rather than personal sentiments.

The truth is, as long as creditors are willing to lend, a debtor won't collapse. Regardless of high interest rates or debt amounts, if creditors maintain faith and continue lending, the debtor can survive.

The US's potential collapse isn't about the amount of debt, but rather when creditors might stop lending. While the US may be heading towards an endpoint, it's unlikely to happen in the near future. Why?

Because major creditors can't afford to let the US fail yet.

The largest US creditors, like Social Security and the Federal Reserve, are domestic and under US control.

Foreign creditors like China and Japan each hold about $1 trillion in US bonds. China still relies on the US and likely will for another 5-10 years until it can drive internal growth.

The idea that China could crash the US by selling all its bonds overlooks practical questions: Who would buy them? At what price? How much would China lose in this scenario?

Japan, since the Plaza Accord, has been closely aligned with US interests and is unlikely to turn against it.

I return to my original question: Will the US collapse? "It depends on when creditors stop lending to the US"

Consider this: Where else could such large sums be placed with low risk if not in US bonds? As long as there's no alternative market large enough to absorb trillions with comparable low risk, it's unlikely that money will shift away from US bonds dramatically enough to cause a collapse.

Conversely, the US is the only major power with interest rates as high as 3%, while the Eurozone, UK, and Japan have near-zero rates. While raising rates increases US debt and burden, it also attracts creditors fleeing from other countries' bonds.

The US's greatest strength is “trust”. As long as this trust persists, the US won't collapse. But if this trust ever disappears, it could trigger the most severe crisis in world history.

However, as I mentioned earlier, I don't think this will happen soon. At the very least, a US crisis is unlikely to precede potential crises in Japan or the Eurozone.

PS. Consider this hypothetical: If Japan or the Eurozone were to face bankruptcy tomorrow, where else could their creditors move such large sums with comparable safety, if not to US bonds?

PS. To clarify, I'm not saying the US is invincible. Throughout history, global powers have risen and fallen: Portugal, Spain, Netherlands, France, Britain, the US, and potentially China in the future. The US will likely fall one day, but there are no clear signs of this happening imminently.

The Demise of the Pension System

December 2019

Recent news about the collapse of the Netherlands' world-renowned pension system highlights a growing global issue. The causes - low birth rates, an aging society, and negative bond yields in Europe - have led to a shortage in Dutch pension funds, potentially forcing benefit cuts or increased contributions.

This problem is more significant than many realize. When Thailand's Social Security Office requested increased contributions, public backlash was swift. I've been discussing the risk of global pension fund deficits and potential bankruptcies for the past three years, affecting countries from the Netherlands to Japan, the United States, and even Thailand.

This issue is crucial because pension funds are a socialist mechanism supporting the capitalist system in an era of increasing wealth concentration. If this mechanism fails, the resulting global economic problems will be severe and far-reaching, affecting a much larger population than previous crises like the subprime mortgage crisis or the dot-com bubble.

When grassroots citizens lose the welfare supporting their lives, demands for government assistance and conflicts with capitalists will arise. (This scenario, predicted by Marx long ago, has been dismissed by capitalists for a century.)

Hong Kong serves as a case study. When citizens reject the existing economic system, chaos ensues. A government losing public trust can trigger economic collapse.

We've seen the US, Europe, and Japan print money without causing the feared hyperinflation, mainly due to sustained confidence in these states. However, when the pension fund crisis hits, this confidence will rapidly erode. The accumulated sins of neo-Keynesian economic stimulus will come back to haunt governments.

When social safety nets disappear for the masses, calls for government intervention and clashes with the wealthy elite will intensify. This scenario, long predicted by Marx and long dismissed by capitalists, may finally come to fruition.

This could lead to the most severe economic collapse in history.

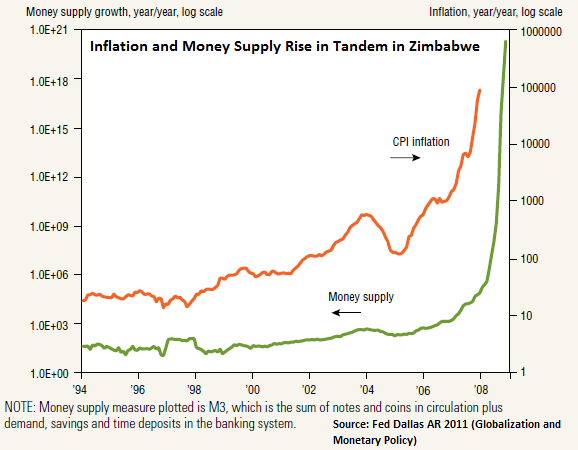

Hyperinflation vs. Inflation

December 2019

Hyperinflation vs. Inflation, what's the Difference?

This post was originally made before the crypto bubble burst in late 2017, but it's worth revisiting.

Zimbabwe's severe hyperinflation in 2017 differed from its 2008 crisis. In 2017, the new Zimbabwean dollar was pegged to the US dollar, limiting money supply to avoid repeating the 2008 scenario. However, when Mugabe's government ran out of money and people feared history repeating, they abandoned the new Zimbabwean dollar for other assets.

The 2008 hyperinflation occurred because: Increased money supply -> Currency devaluation -> People abandoning the currency

The 2017 inflation began because: Fear -> People starting to abandon the currency (despite unchanged money supply)

When the new government replaced Mugabe, confidence returned and inflation decreased because: Confidence -> People retaining currency

Fundamentally, inflation and hyperinflation are quite different. Some think hyperinflation is just extreme inflation, but regular inflation typically results from changes in demand/supply, while hyperinflation stems from a loss of public trust in the state.

Therefore, the reason hyperinflation can decrease rapidly is because the opposite occurs: confidence in the state is restored.

Cryptocurrencies started with a similar concept, controlling scarcity through limited supply (e.g., Bitcoin's 21 million coin limit). However, scarcity is just one factor in building trust. Even if an medium of exchange has scarcity, it's useless without trust.

This is the reason I believe Bitcoin will persist, as long as people trust it. It's not that it will continue to exist simply because it has a limited supply (even with limited supply, if people don't trust it, it will collapse). However, other digital currencies, even though they may have limited supply (like the new Zimbabwean dollar), if people don't trust them at all, everything can come to an end.

Is there anything in the world that lacks economic value but people still want to possess? The answer is "yes," and such things retain value as long as people value them (like artpiece). However, I believe digital assets can never have this property (despite uniqueness and limited supply, they lack aesthetic value).

In my opinion, if digital currencies aren't used for real-world transactions and lack economic value, trust is likely to disappear. When it does, it won't be gradual but sudden, like hyperinflation in fiat currencies. This day seems to be approaching (I said this before the crypto bubble burst in late 2017).

PS. (2019 Update) The Zimbabwean dollar is nearing hyperinflation again, with the same old problem of declining trust in government.

PS. (2024 Update) Post-COVID-19 Update on Zimbabwean Currency. In the aftermath of the COVID-19 crisis, the Zimbabwean dollar collapsed again. In 2024, the government introduced a new currency backed by gold reserves. It remains to be seen whether this move will restore public confidence in the nation's currency.

PS. There's an extreme opposite example: a country that prints money excessively, where "money supply" is just a concept for this currency, yet people's trust remains unshaken.

In conclusion, trust is everything; scarcity is just a myth. If you hold crypto because you believe in scarcity, please reconsider. But if you hold it because you believe people trust it, carry on.

Will the Welfare State Really Save Capitalism?

December 2019

Recent crises in social security and pension systems, exacerbated by the aging society, raise the possibility of these welfare states becoming "deficit" or even "bankrupt" in the future.

The welfare state was initially created to support capitalism, reducing the inequality between "Bourgeoisie (Capitalist class)" and "Proletariat (Working class)" during the early Industrial Revolution. In Manchester, England, a textile industry hub, the average life expectancy was only 42 years due to harsh working conditions, including 80-100 hour work weeks and child labor.

As capitalism degraded quality of life, Marxism became an alternative for Europeans. Communists later adapted Marxism, distorting it beyond recognition from Karl Marx's original ideas.

To prevent its collapse, capitalism compromised between capitalists, the state, and workers. This led to basic welfare states during the Industrial Revolution, initiating labor and public health reforms. (The UK's Labour Party originated from these struggles.)

Some say that the welfare state is the meeting point between capitalism and socialism, or the center between left and right. It sounds fancy and appealing.

But is it really like that in reality...?

Simple math shows that since the 2008 US subprime crisis, global money supply has increased rapidly due to massive QE by major economic powers. However, most people haven't become richer at the same rate, indicating that most new money flows to a small minority, challenging the 80/20 Pareto principle (now approaching a 99/1 ratio).

Elementary math proves that if most money isn't in the hands of the majority, creating a welfare state by "setting aside" money from the majority for investment can't match the wealth flowing to the world's elite.

You're a piece on a Monopoly board where every space already has someone else's hotel. Even if you complete a lap and collect $2,000 for passing "Go", it won't be enough to help you survive on this Monopoly board.

In simpler terms, we can't achieve greater equality through the welfare state system unless the upper class willingly reduces their wealth (e.g., significantly higher taxes on the rich to fund welfare for the majority, which rarely happens). The state's most crucial role is successfully extracting wealth from the rich to serve as new input for the welfare state, which is an extremely challenging task.

Ultimately, the distortions of capitalism and changing demographics are causing the welfare state, capitalism's last hope, to collapse.

This doesn't even account for the planet's deteriorating health due to capitalism's exploitation of resources for wealth creation, leaving Earth with little chance to return to its past prosperity.

We see Bill Gates recommending the book "Factfulness: Ten Reasons We're Wrong About the World - Why Things Are Better Than You Think.” Do we really think this planet is better every day as the book claims...?

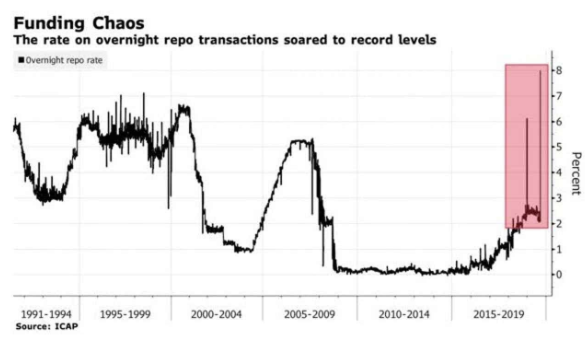

The FED’s Intervention in the Repo Market

A Silent Threat | December 2019

The Federal Reserve's intervention in the overnight repo rates is quietly alarming.

The spike in repo rates over recent months indicates a lack of trust among major banks (causing overnight interbank lending rates to jump dramatically, forcing the FED to inject money to push rates down).

They say it takes one to know one. Big banks likely know each other's true nature.

If banks don't trust each other, there must be a significantly frightening reason behind it.

Is there a hidden risk in the US banking sector waiting to explode?

This intervention is unlikely to end easily. They plan to inject about $500 billion this year, with possible continuation next year, suggesting this isn't a short-term problem.

A bedtime conspiracy theory. I actually have no data. It's like a Hidden Markov Model - we only see small bits of information but must guess what's really hiding behind it.

I don't mean to cause undue worry. There might be nothing to it. But it's worth keeping an eye on this situation.

What is Repo market?

The Repo market, or repurchase agreement market, is a place where banks and financial institutions borrow short-term money from each other, typically overnight. Here's how it works: the borrower sells securities (like government bonds) to the lender and agrees to buy them back the next day at a slightly higher price. The difference in price is essentially the interest rate. The Repo market is crucial because it helps banks manage their short-term liquidity and is an important mechanism for central banks to control interest rates.

The spiking of the repo rates is not a good sign for several reasons:

- Indicates liquidity problems: A spike in repo rates suggests banks are in greater need of cash and are willing to pay higher interest to get it.

- Reflects lack of confidence: Banks may be unwilling to lend to each other due to concerns about counterparty risk.

- Impacts other financial markets: Higher repo rates can lead to higher borrowing costs in other markets.

- Signals potential broader financial system issues: It may be a sign of deeper problems in the banking system.

- Challenges monetary policy: It forces central bank intervention, which can affect overall monetary policy.

Universal Basic Income (UBI)

What Is It Really For? | February 2020

I was shocked today reading a post about Finland's Basic Income experiment. Many people, even media outlets covering this topic, seem to think Basic Income was designed to solve unemployment issues.

However, the measure of Basic Income's success isn't "Did unemployment rates decrease?" Basic Income isn't about creating more jobs. It's about ensuring that even as our world moves towards an era with fewer jobs, humans can still survive and thrive!

This indicates that "regular salary man" may no longer be essential for survival in the future.

In capitalism, we've been conditioned to follow a life path: birth, education, work, family, retirement, death. This has been the norm for hundreds of years because without work, you can't support yourself or your family.

Capitalist thinking has ingrained the idea that a good economy means low unemployment, everyone should have a job, and that's how a nation prospers.

But what have we seen in the 250 years since the Industrial Revolution, alongside increased so-called "Civilization"?

We see a deteriorating world - we now need masks to go outside, oceans are polluted with plastic, forests are disappearing, air pollution is severe, over 15% of the world's population is starving. Those who can afford food consume carcinogenic agents. We ingest chemicals from production processes daily - paraquat, pesticides, antibiotics from animals. Rates of depression, mental health issues, and stress are skyrocketing.

What quality of life will our descendants face if capitalism continues on this path?

Let's reimagine our world through a different lens…

What if people didn't have to work just to survive, but had enough money to live on? How could we use our free time to make the world better?

Imagine waking up each day, not worried about making ends meet, but excited to help others and our planet. Could we spend more time volunteering, cleaning up nature, or coming up with ideas to solve big problems?

Can we restore prosperity to this planet? The prosperity we've almost completely destroyed in the capitalist era?

Can we bring back the health and beauty our world once had? Can we heal the damage done by years of taking too much from nature?

What if we created new kinds of jobs? Jobs that don't just pay bills, but make life better for everyone. What amazing things could we do if we worked because we wanted to, not because we had to?

In this new world, could we measure a person's worth by how much they help others, not by how much money they have? Could we value kindness and good deeds more than wealth?

This is what Universal Basic Income is really about. It's not just about unemployment numbers. It's about rethinking what it means to be human and how we can all contribute to a better world.

When we talk about Basic Income, let's think big. Let's imagine a world where everyone has the chance to make a difference, not just survive. A world where our only limits are our imagination and our care for each other.

PS. I haven't addressed how the state will fund Basic Income (I'll explain that in other posts). Let's focus on measuring the "success" of Basic Income first.

For those unfamiliar with the UBI concept, please read below.

What is UBI?

Elon Musk told the media that it's highly likely our world will enter the era of Universal Basic Income (UBI).

UBI is a new form of welfare where the state provides a minimum income to all citizens. The main reason is that in the future, automation systems will replace human labor in many job positions (it's said that in 20 years, up to 80% of human jobs may be replaced by automation and AI). This includes drivers, waiters, farmers, factory workers, receptionists, ticket sellers, cashiers, stock analysts, stock brokers, etc.

When people lose jobs to machines, there will be severe unemployment, even though the world's production costs will decrease dramatically. But citizens won't have purchasing power, leading to chronic deflation (similar to the Great Depression of 1929).

During the Great Depression, the problem was solved using Keynesian economics - the government injected money to stimulate the economy, build infrastructure, create jobs. When people had jobs and salaries, spending would circulate, eventually reviving the economy.

But in the near future, the Keynesian approach may not work because future "jobs" won't necessarily need humans. So increasing "jobs" by the state may not be the solution.

Many AI scientists, including Elon Musk and Andrew Ng, suggest that the solution to severe deflation caused by automation disrupting human labor is to "just give money to the people"!

This is UBI.

But economists ask: Where will the state get money for UBI? Theoretically, there are quite clear solutions that seem possible in the near future. I'll explain this another time.

Global Pension Funds

Shifting Strategies in Low-Interest Environments | February 2020

An intriguing trend is emerging among the world's largest pension funds, highlighting a stark contrast between Asian and American investment strategies. Let's examine the top five:

- Social Security Trust Funds (US)

Assets: $2.9 trillion

Strategy: Nearly 100% invested in US Treasury bonds - Government Pension Investment Fund Japan (Japan)

Assets: $1.5 trillion

Strategy: Reducing bond holdings, increasing investments in stocks and alternative assets - Military Retirement Fund (US)

Assets: $0.8 trillion

Strategy: Almost entirely invested in US Treasury bonds - Federal Employees Retirement System (US)

Assets: $0.7 trillion

Strategy: Predominantly invested in US Treasury bonds - National Pension Service of Korea (South Korea)

Assets: $0.7 trillion

Strategy: Reducing bond holdings, increasing investments in stocks and alternative assets

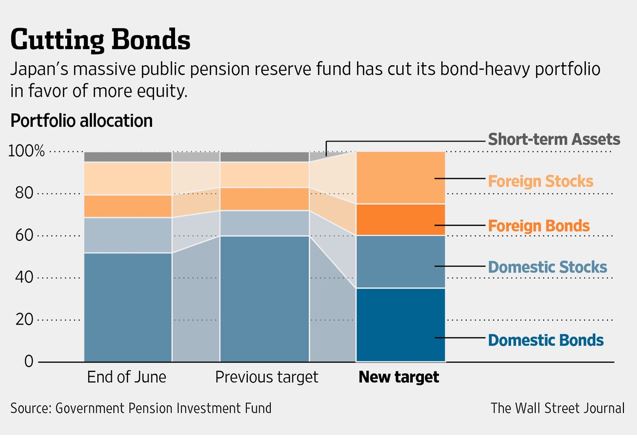

The divergence between Asian and American approaches is striking. Asian funds, particularly in Japan and South Korea, are actively reducing their bond holdings and diversifying into other asset classes to boost returns, albeit with increased risk. Japan's GPIF has been particularly aggressive, significantly cutting its Japanese government bond holdings and raising its stock allocation from 10% to 25%.

In contrast, US funds remain steadfast in their commitment to Treasury bonds, despite rock-bottom interest rates. This raises an important question: How will the US address the challenges facing pension funds in an aging society with persistently low returns?

PS. It's worth noting that if pension funds and Sovereign Wealth Funds worldwide continue to shift investments from low-risk bonds to stocks and alternative assets, we may see sustained growth in global stock markets (with some exceptions like Thailand Stock Exchange). This trend suggests that as long as interest rates remain low, more capital will flow into stock markets, even if corporate earnings don't meet expectations.

PS. Regarding Sovereign Wealth Funds (SWFs), which typically have higher risk tolerances than pension funds, we observe an increasing trend in alternative asset allocation, particularly among Asian SWFs.

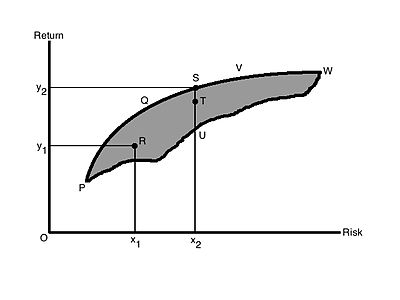

The Hidden Peril of Risk-Free Government Bonds

A Critical Look at Modern Portfolio Theory | February 2020

The most alarming aspect of current risk management and asset allocation mechanisms is the assumption that government bonds carry zero risk. This belief, rooted in the notion that states cannot fail, has led to asset diversification strategies revolving around the bond market, which is widely considered "low-risk, low-return."

I've consistently argued that Modern Portfolio Theory (MPT) has a significant flaw. The issue isn't with the theory itself, but with the concept of measuring expected risk and return based on historical data. We simply "believe" that bonds are safe because they have been in the past, assuming this will remain unchanged in the future. (For those interested in this concept, I recommend reading about the turkey problem in Nassim Taleb's "The Black Swan".)

People perceive bonds as low-risk primarily due to state stability. But what if we wake up tomorrow to find bonds have become high-risk, low-return assets?

As mentioned in previous posts, major powers like Japan (and even the US and Eurozone) share a common problem: market distortion through central bank intervention. The bond market has been increasingly divorced from reality over the past decade or more.

The challenge in risk assessment lies in how much additional information we incorporate into our models and whether this new data allows us to recalibrate our perception of bond risk.

Using historical variance to predict future risk is akin to driving a car with the windshield covered, relying solely on the rearview mirror for navigation. Yet, most financial experts believe this backward-looking approach will safely lead us to our destination.

PS. I'm hopeful that the asset risk assessment model our Avareum team is researching, using causal inference and deep learning, might provide answers to the asset allocation questions that have long puzzled me.

About The Author

Pravithana Niran

CEO & Founder of Avareum Capital Fund

Pravithana Niran has spent the past 15 years working as an economist and 20 years as a tech entrepreneur, bringing together insights from both fields in his approach to finance and technology. He is the founder of Avareum Capital Fund, a digital asset hedge fund, and Avareum Research, which explores applications of AI in finance.

Niran has written several books on economics and investment, aiming to share his understanding of macroeconomics, digital assets, and emerging technologies. His work with Avantis Laboratory focuses on asset tokenization, reflecting his interest in the potential of blockchain in finance.

Disclaimer: Avareum Research is an independent crypto research firm committed to providing unbiased and informative content. While we strive for complete objectivity, it's important to note that the research industry is inherently complex and may be influenced by various factors. To ensure transparency, we disclose any potential conflicts of interest, such as financial sponsorships or investments in the crypto space. Ultimately, all research and analysis provided by Avareum Research is intended for informational purposes only and should not be considered financial advice. Please consult with a qualified professional before making any investment decisions.

© 2024 Avareum Research. All Rights Reserved. This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.