Japan's Government Pension Investment Fund (GPIF) Explores Bitcoin Investment Amidst Aging Population Crisis

ข่าวเรื่อง GPIF หรือกองทุนบำเหน็จบำนาญของญี่ปุ่น ศึกษาการลงทุน Bitcoin เป็นประเด็นที่น่าสนใจ ซึ่งเกี่ยวโยงไปกับประเด็นปัญหาเศรษฐกิจหลักของญี่ปุ่นคือ วิกฤติประชากรสูงวัย (aging population crisis)

เรื่องของ aging society นั้นถูกพูดถึงกันมานานแล้ว อ้างอิงจากเว็บไซต์ populationpyramid ประมาณการกันว่าในปี 2100 ประชากรไทยจะลดจำนวนลงจาก 68 ล้านคนมาอยู่แถวๆ 40 ล้านคน (-41%) ส่วนญี่ปุ่น ประชากรจะลดจาก 127 ล้านคน เหลือเพียงแค่ 83 ล้านคน (-34%)ในขณะที่ประเทศพัฒนาแล้วส่วนใหญ่ประชากรมีจำนวนลดลงเนื่องจากอัตราการเกิดต่ำมากจากค่านิยมของคนยุคใหม่ที่ไม่นิยมการมีบุตร และอัตราการตายต่ำจากพัฒนาการของเทคโนโลยีทางการแพทย์ ในขณะที่ประเทศในกลุ่มแอฟริกากลับมีอัตราการเกิดที่เพิ่มขึ้นอย่างรวดเร็ว ทำให้โครงสร้างประชากรในอนาคตเปลี่ยนแปลงแตกต่างกันมากในแต่ละทวีป

ลองคิดภาพนะครับว่า ในประเทศญี่ปุ่นที่อัตราการเกิดต่ำมาก คนวัยแรงงานลดน้อยลง ทำให้รัฐบาลขาดรายได้จากการเก็บภาษี รวมไปถึงรายได้ของระบบบำเหน็จบำนาญก็จะขาดหายไปอย่างมากแถมยังต้องเจอกับปัญหาเรื่องการเพิ่มปริมาณของประชากรวัยเกษียณ เมื่อคนเกิดน้อยลง รัฐขาดรายได้ แต่ตรงกันข้ามคนวัยเกษียณกลับเพิ่มขึ้น

วิบากกรรมซ้ำกองทุนบำเหน็จบำนาญของประเทศญี่ปุ่นอีกต่อหนึ่ง ก็คือเงินกองกลางที่กองทุนบำเหน็จบำนาญเก็บเอาไว้ จำเป็นจะต้องหาผลตอบแทนที่ความเสี่ยงต่ำ ส่วนใหญ่กองทุนบำเหน็จบำนาญจึงมักจะปล่อยกู้ให้กับรัฐบาลในรูปแบบของการซื้อพันธบัตร แต่อัตราผลตอบแทนพันธบัตรรัฐบาลญี่ปุ่นกลับอยู่ในระดับ 0% มายาวนานร่วมทศวรรษ นั่นหมายความว่า เจ้าหนี้อย่างกองทุนบำเหน็จบำนาญไม่เพียงแต่จะได้ผลตอบแทนต่ำลงเรื่อยๆ ยังจะเจอสถานการณ์ที่เงินต้นลดลงจากอัตราดอกเบี้ยแท้จริงที่ติดลบซะอีก และนี่เป็นระเบิดเวลาก้อนใหญ่ที่ซ่อนอยู่ในระบบบำเหน็จบำนาญของประเทศญี่ปุ่น (รวมถึงประเทศพัฒนาแล้วแทบทุกประเทศ)

รายได้น้อยลงฮวบฮาบ รายจ่ายเพิ่มขึ้นปรี้ดๆ แถมเงินกองกลางที่มีก็ผลตอบแทนต่ำติดดิน ถ้าปล่อยให้เป็นแบบนี้ต่อไป ระบบบำเหน็จบำนาญของประเทศพัฒนาแล้วทั่วโลกก็จะเข้าสู่ภาวะล้มละลายในที่สุด

กองทุนบำเหน็จบำนาญของญี่ปุ่น (GPIF) ที่มนุษย์เงินเดือนหรือ "ซารารีมัง" ของญี่ปุ่นแบ่งเงินไปฝากไว้ทุกปีๆ ฝากมาตลอดชีวิต กลับเริ่มประสบปัญหา เงินของประชาชนไม่สร้างผลตอบแทนให้กองทุนอย่างที่ควรจะเป็น

เพราะอะไร..?

เพราะ GPIF ซื้อแต่พันธบัตรรัฐบาลที่ให้ดอกเบี้ยลดลงเรื่อยๆ จนเข้าขั้นติดลบไปแล้ว..!! ถ้าดอกติดลบ แปลว่าเงินที่เหล่าซารารีมังหามาอย่างยากลำบากตลอดชีวิตที่เก็บอยู่ในกองทุนจะลดลงเรื่อยๆ ตามระยะเวลาที่ถือพันธบัตร

ช่วงก่อนปี 2014 GPIF เจอปัญหาร้ายแรงจากดอกเบี้ยพันธบัตรที่ติดลบ เมื่อผลตอบแทนของกองทุนลดลงเรื่อยๆ ทำให้ความมั่นใจของประชาชนที่มีต่อสวัสดิการของตนเองในอนาคตก็จะยิ่งแย่ลง..แก่แล้วรัฐจะเลี้ยงดูชั้นได้มั้ยนะ..? ถ้าระบบบำเหน็จบำนาญล้มละลาย ชั้นจะทำยังไงนะ..?

ซ้ำร้ายเงินเก็บของประชาชนญี่ปุ่นส่วนใหญ่ก็ไปลงทุนซื้อพันธบัตรรัฐบาลน่ะแหละ หรือพูดอีกแง่ก็คือ ประชาชนก็คือเจ้าหนี้ของรัฐบาลเอง (จุดนี้เป็นจุดที่ญี่ปุ่นแตกต่างจากชาติอื่นตรงที่ชาติอื่นนี่เจ้าหนี้มักจะไม่ใช่คนในประเทศแต่เป็นต่างชาติ ถ้านึกภาพไม่ออก ลองมองดูเมืองไทย มีประชาชนไทยคนไหนเคยซื้อพันธบัตรรัฐบาลไทยมั้ยล่ะ..? น่าจะพอเห็นภาพนะครับ)

กองทุนบำเหน็จบำนาญที่พึ่งวัยชราผลตอบแทนก็ต่ำ แถมเงินเก็บก็ดันเอาไปซื้อพันธบัตร ซึ่งดอกเบี้ยก็ต่ำอีก ถ้าคุณเป็นคนญี่ปุ่น จะทำยังไง..?

พอความไม่มั่นใจในอนาคตเพิ่มขึ้นเรื่อยๆ คนจะยิ่งเก็บเงินไม่ใช้จ่าย, การลดดอกเบี้ย แทนที่จะเพิ่มความเชื่อมั่นให้ประชาชน กลับให้ผลตรงกันข้ามเฉยเลย เมื่อถึงจุดหนึ่ง GPIF อาจจะเข้าสู่ความเสี่ยงที่จะล้มละลาย (ค่าใช้จ่ายสวัสดิการมากกว่าเงินที่มีในกองทุน) สังคมผู้สูงอายุมาถึงแล้วครับ คนวัยทำงานส่งเงินเข้ากองทุนลดลงเรื่อยๆ เพราะประชากรวัยทำงานหายไป, แต่คนใช้เงินจากกองทุนบำเหน็จบำนาญเพิ่มขึ้นเรื่อยๆ เพราะประชากรวัยเกษียณเพิ่มมากขึ้นทุกวันรายรับลดลง รายจ่ายเพิ่มเงิน, แถมรายรับที่มีอยู่ ดันไม่สร้างผลตอบแทนที่ดีพออีก

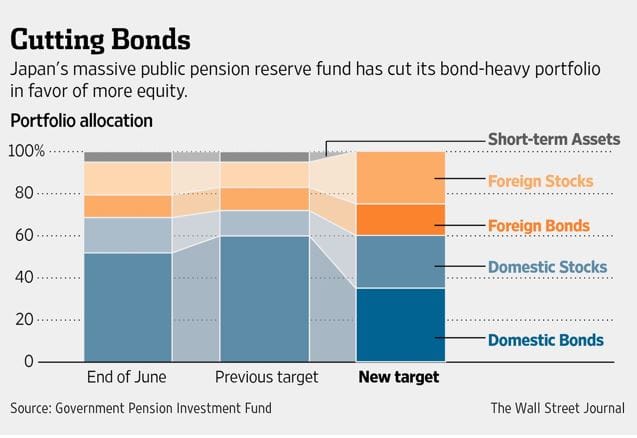

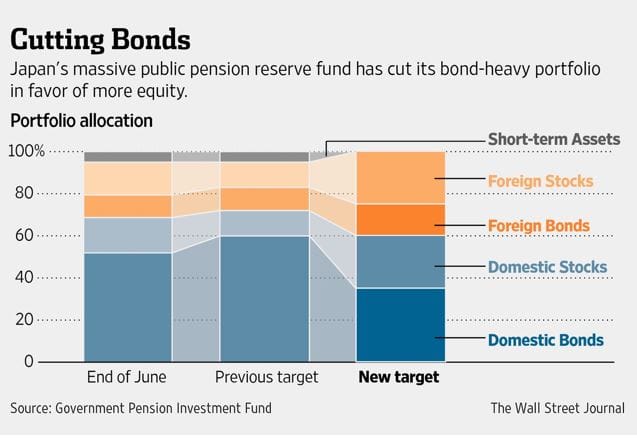

ในปี 2014 กองทุนบำเหน็จบำนาญของประเทศญี่ปุ่นที่มีขนาดกองทุน $1.2 ล้านล้านเหรียญสหรัฐ ก็เลยเริ่มนโยบายลดการถือพันธบัตรรัฐบาล และเพิ่มสัดส่วนการลงทุนในสินทรัพย์เสี่ยงเพิ่มขึ้น โดยจัดสรรเงินทุนไปลงทุนในหุ้นญี่ปุ่นเพิ่มจาก 12% เป็น 25% หรือย้ายไปถือหุ้นถึง 1 ใน 4 ของกองทุน!! (และนี่เป็นเหตุผลหนึ่งที่ Nikkei วิ่งขึ้นมาเยอะมากในช่วง 2014-2015)

แต่แน่นอนว่าการตัดสินใจทางเลือกนี้ย่อม ‘เพิ่มความเสี่ยง’ ให้กับกองทุนอย่างเลี่ยงไม่ได้ ถ้าตลาดหุ้นพัง นั่นหมายถึงเงินของประชาชนจะหายไปทันที (Nikkei มี market cap ลดลงเกือบ 30% ในช่วงปลายปี 2015 ถึงกลางปี 2016 แน่นอนว่าเงินกองกลางของ GPIF ก็ลดลงตามไปด้วยไม่มากก็น้อย)

แต่เมื่อเวลาผ่านมาเกือบสิบปี การตัดสินใจของ GPIF ให้คำตอบชัดเจนว่าเป็นทางเลือกที่ถูกต้อง หลังจากที่ NIKKEI ปรับตัวทำ new all time high ที่ 40,000 จุดในเดือนมีนาคม 2024 นี้ ทำให้ผลตอบแทนของ GPIF เพิ่มขึ้นอย่างก้าวกระโดด โดยทำกำไรได้ถึง 232 ล้านเหรียญสหรัฐในปี 2023

ไม่เพียงแค่นั้น ในปี 2024 นี้ทาง GPIF เริ่มมองหาช่องทางการลงทุนกับสินทรัพย์ทางเลือกเพิ่มเติม อย่าง Bitcoin เป็นการแสดงให้เห็นถึงความเข้าใจปัญหาเรื่องวิกฤติ aging society ที่จะมีผลต่อกองทุนบำเหน็จบำนาญ และแม้จะเป็นทางเลือกที่ดูจะมีความเสี่ยง แต่ในมุมมองของเรา นี่เป็นทางเลือกเดียวที่กองทุนบำเหน็จบำนาญจะสามารถสร้างผลตอบแทนที่สูงขึ้นในช่วงภาวะที่มีความจำเป็นจะต้องปรับเปลี่ยนกลยุทธ์การลงทุนให้สอดคล้องกับโครงสร้างประชากรในยุคปัจจุบัน

ไม่เพียงแต่ GPIF ของญี่ปุ่นเท่านั้น แต่กองทุนบำเหน็จบำนาญหลายประเทศในโลกก็เริ่มมีการ diversify การลงทุนไปยังสินทรัพย์เสี่ยงและสินทรัพย์ทางเลือกมากขึ้นเรื่อยๆ เช่น เกาหลี สิงคโปร์ และหลายประเทศในตะวันออกกลาง

ส่วนผลลัพธ์จะเป็นคำตอบที่ถูกต้องหรือไม่ บางทีเราอาจจะไม่ต้องรอถึง 10 ปี แบบที่ GPIF ของญี่ปุ่น เคยทำได้สำเร็จในการทิ้งพันธบัตรรัฐบาลมาลงทุนในตลาดหุ้นก็เป็นได้

The recent news of Japan's Government Pension Investment Fund (GPIF) considering an investment in Bitcoin has sparked significant interest, particularly in light of the country's long-standing economic challenge: the aging society crisis.

The aging society problem has been a topic of discussion for many years. According to projections from the website populationpyramid, by 2100, Thailand's population is expected to decrease from 68 million to around 40 million (-41%), while Japan's population will decline from 127 million to just 83 million (-34%). Most developed countries are experiencing population declines due to extremely low birth rates, influenced by the values of younger generations who are less inclined to have children, and low death rates resulting from advancements in medical technology. In contrast, countries in Africa are witnessing a rapid increase in birth rates, leading to significant disparities in population structures across different continents in the future.

Imagine a scenario in Japan, where the birth rate is extremely low, and the working-age population is diminishing. This leads to a decrease in government revenue from tax collection and a substantial loss of income for the pension system. Simultaneously, the country faces the challenge of an increasing number of retirees. As fewer people are born, the government loses revenue, while the population of retirees continues to grow.

To compound the misfortune, Japan's pension funds face another dilemma. The funds collected by pension funds need to seek low-risk returns, and most pension funds typically lend money to the government by purchasing government bonds. However, the yield on Japanese government bonds has remained at 0% for over a decade. This means that creditors, such as pension funds, not only face declining returns but also encounter situations where the principal amount decreases due to negative real interest rates. This is a ticking time bomb hidden within Japan's pension system, a problem shared by most developed countries.

With dwindling revenues, soaring expenses, and low-yielding central funds, if left unchecked, the pension systems of developed countries worldwide could eventually face bankruptcy.

Japan's Government Pension Investment Fund (GPIF), where Japanese salaried workers or "sarariman" contribute a portion of their income every year throughout their lives, is beginning to face challenges. The money entrusted by the public is not generating the expected returns for the fund.

Why is this happening?

It's because GPIF has been primarily investing in government bonds, which have been offering declining interest rates, even reaching negative levels. When interest rates turn negative, it means that the hard-earned money that the sarariman have saved in the fund throughout their lives will gradually decrease over the duration of holding the bonds.

Before 2014, GPIF faced severe problems due to negative bond yields. As the fund's returns continued to decline, public confidence in their future welfare also deteriorated. People started questioning whether the government would be able to support them in their old age and what would happen if the pension system went bankrupt.

To make matters worse, most of the Japanese public's savings are invested in government bonds. In other words, the public is essentially the government's creditor. (This is where Japan differs from other countries, where creditors are often foreign entities rather than domestic citizens. If you're having trouble visualizing this, consider Thailand – how many Thai citizens have ever purchased Thai government bonds? This should help you understand the picture.)

The pension fund that people rely on for their old age has low returns, and the savings are invested in bonds with low interest rates. If you were Japanese, what would you do?

As uncertainty about the future increases, people tend to save more and spend less. Instead of boosting public confidence, lowering interest rates has the opposite effect. At some point, GPIF may face the risk of bankruptcy (when welfare expenses exceed the fund's available assets). The aging society has already arrived. The number of working-age people contributing to the fund is steadily decreasing due to the shrinking working-age population, while the number of people drawing from the pension fund is continuously increasing as the retired population grows daily. Revenues are falling, expenses are rising, and the existing income fails to generate sufficient returns.

In 2014, Japan's Government Pension Investment Fund, with a fund size of $1.2 trillion, initiated a policy to reduce its holdings of government bonds and increase its exposure to riskier assets. The fund allocated more capital to Japanese stocks, increasing the proportion from 12% to 25%, effectively shifting 1 in 4 of the fund's assets to equities! (This is one of the reasons why the Nikkei index experienced a significant surge during 2014-2015.)

However, it is undeniable that this decision inevitably 'increased the risk' for the fund. If the stock market crashes, it would mean an immediate loss of public funds. (The Nikkei's market cap decreased by nearly 30% from late 2015 to mid-2016, and naturally, GPIF's central funds also declined to some extent.)

But as almost a decade has passed, GPIF's decision has clearly proven to be the right choice. After the Nikkei hit a new all-time high of 40,000 points in March 2024, GPIF's returns have skyrocketed, with profits reaching $232 billion in 2023.

Furthermore, in 2024, GPIF has started exploring additional alternative investment opportunities, such as Bitcoin. This demonstrates their understanding of the impact of the aging society crisis on pension funds. Although it may seem like a risky choice, in our view, it is the only option for pension funds to generate higher returns during a period when it is necessary to adapt investment strategies to align with the current demographic structure.

GPIF is not alone in this approach. Pension funds in many countries around the world are increasingly diversifying their investments into riskier assets and alternative investments, such as South Korea, Singapore, and several Middle Eastern countries.

As for whether the outcome will prove to be the right answer, perhaps we won't have to wait 10 years, as Japan's GPIF has already successfully demonstrated by shifting from government bonds to stock market investments.

Disclaimer: Avareum Research is an independent crypto research firm committed to providing unbiased and informative content. While we strive for complete objectivity, it's important to note that the research industry is inherently complex and may be influenced by various factors. To ensure transparency, we disclose any potential conflicts of interest, such as financial sponsorships or investments in the crypto space. Ultimately, all research and analysis provided by Avareum Research is intended for informational purposes only and should not be considered financial advice. Please consult with a qualified professional before making any investment decisions.

© 2024 Avareum Research. All Rights Reserved. This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.