The Demographic Challenge Facing Social Security

โพสนี้ผมอยากพูดถึงความเสี่ยงที่กองทุนประกันสังคม (ทั่วโลก) จะต้องเจอในอนาคต เผื่อต่อยอดความคิดของหลายๆ คนที่กำลังให้ความสนใจเรื่องการลงทุนของประกันสังคมมากขึ้นในช่วงนี้ (ซึ่งผมถือว่าเป็นเรื่องที่ดีนะครับ เมื่อก่อนไม่เคยมีใครสนใจเลย ว่าประกันสังคมจะเอาเงินไปลงทุนอะไร ทั้งๆ ที่จริงๆ เงินในนั้นก็เงินพวกเราทั้งนั้น)

ถ้าผมจะเริ่มเรื่องนี้ ต้องบอกว่า ปัญหาของประกันสังคม มันเริ่มต้นจาก aging society ครับ...

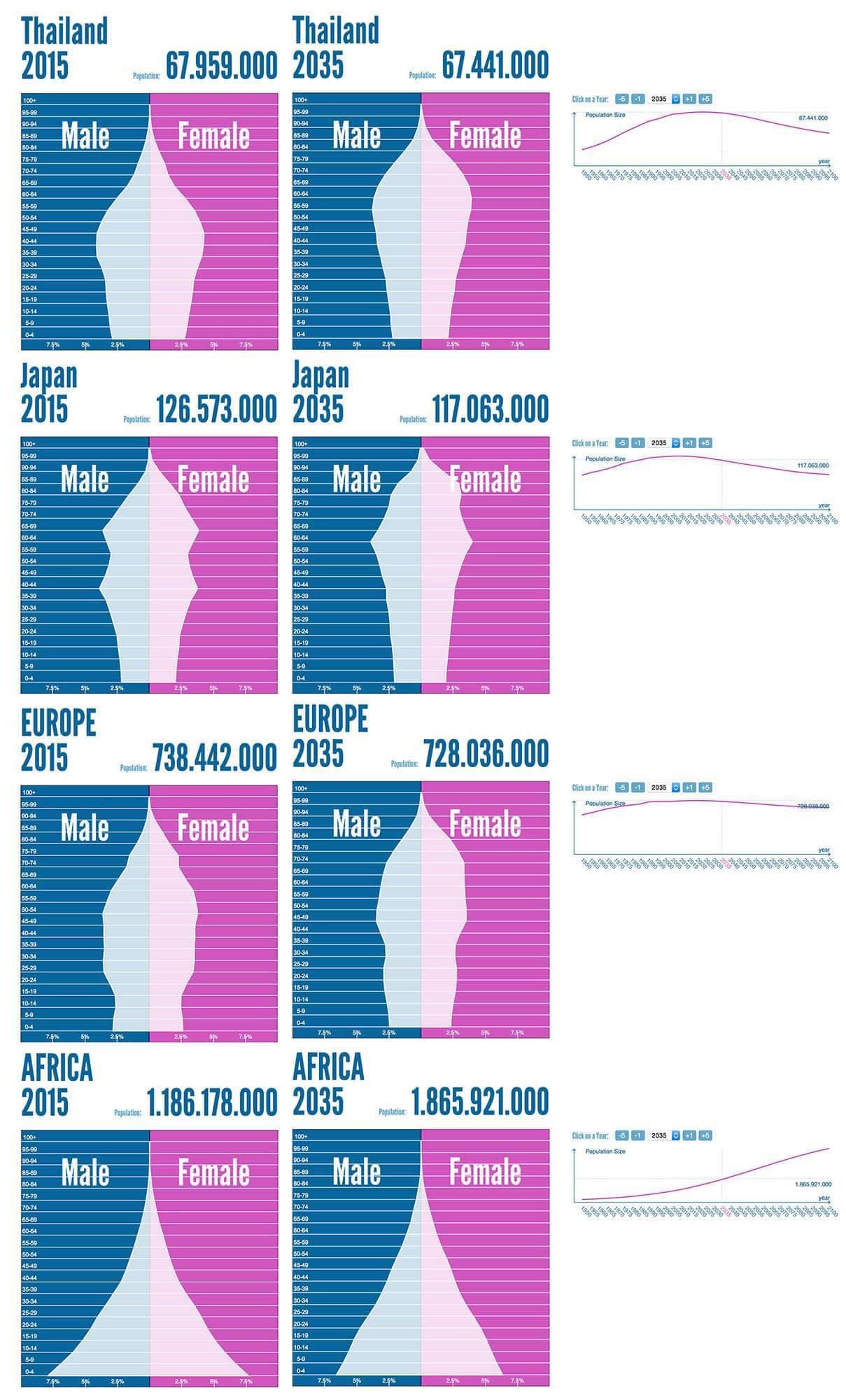

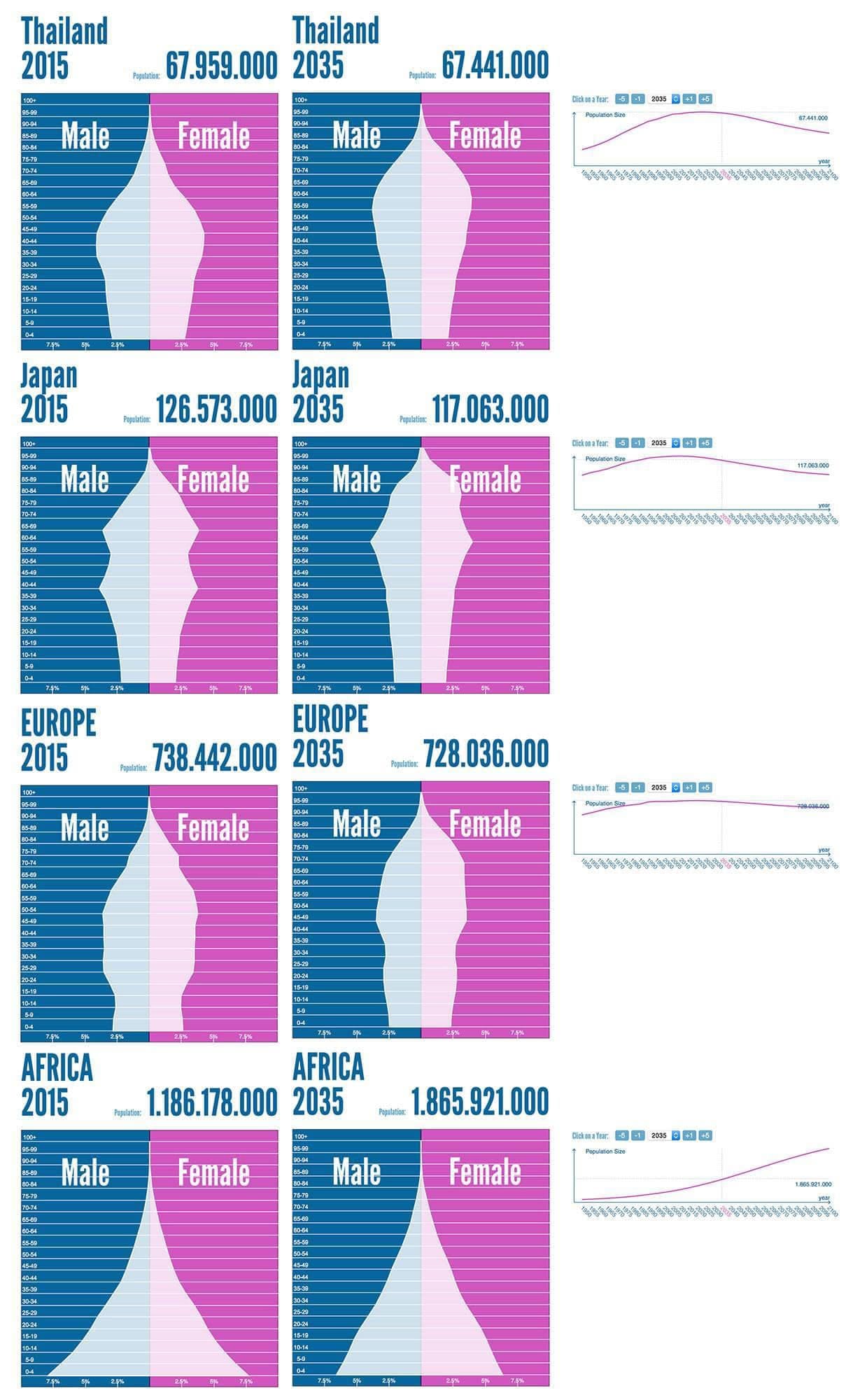

เรื่องของ aging society นั้นถูกพูดถึงกันมานานแล้ว อ้างอิงจากเว็บไซต์ populationpyramid ประมาณการกันว่าในปี 2100 ประชากรไทยจะลดจำนวนลงจาก 68 ล้านคนมาอยู่แถวๆ 40 ล้านคน (-41%) ส่วนญี่ปุ่น ประชากรจะลดจาก 127 ล้านคน เหลือเพียงแค่ 83 ล้านคน (-34%)

ในขณะที่ประเทศพัฒนาแล้วส่วนใหญ่ประชากรมีจำนวนลดลงเนื่องจากอัตราการเกิดต่ำมากจากค่านิยมของคนยุคใหม่ที่ไม่นิยมการมีบุตร และอัตราการตายต่ำจากพัฒนาการของเทคโนโลยีทางการแพทย์ ในขณะที่ประเทศในกลุ่มแอฟริกากลับมีอัตราการเกิดที่เพิ่มขึ้นอย่างรวดเร็ว ทำให้โครงสร้างประชากรในอนาคตเปลี่ยนแปลงแตกต่างกันมากในแต่ละทวีป

ลองคิดภาพนะครับว่า ในประเทศพัฒนาแล้วคนวัยแรงงานไม่มีงานทำ ทำให้รัฐบาลขาดรายได้จากการเก็บภาษี รวมไปถึงรายได้ของระบบประกันสังคมก็จะขาดหายไปอย่างมาก

แถมยังต้องเจอกับปัญหาเรื่องการเพิ่มปริมาณของประชากรวัยเกษียณ เมื่อคนเกิดน้อยลง แถมตกงาน รัฐขาดรายได้ แต่ตรงกันข้ามคนวัยเกษียณกลับเพิ่มขึ้น

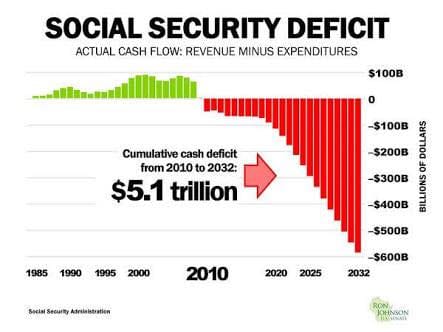

Social Security Trust Fund ของสหรัฐอเมริกาเริ่มเกิดอาการกระแสเงินสดติดลบมาตั้งแต่ปี 2010 (รายได้ที่เก็บจากประชากรวัยแรงงาน น้อยกว่ารายจ่ายที่จ่ายให้กับประชากรวัยเกษียณ ทำให้เกิดงบประมาณขาดดุล) และแนวโน้มว่ากองเงินประกันสังคมขนาด $2.7 ล้านล้านเหรียญอาจจะหมดเกลี้ยงเหลือ 0 ภายในปี 2030 (ซึ่งจริงๆ แล้วการประมาณการนี้ยังไม่ได้คำนวนความเร่งของพัฒนาการเทคโนโลยีที่จะทำให้ประชากรวัยแรงงานตกงานมากขึ้นในสิบปีข้างหน้านี้นะครับ)

วิบากกรรมซ้ำกองทุนประกันสังคมของประเทศพัฒนาแล้วอีกต่อหนึ่ง ก็คือเงินกองกลางที่ประกันสังคมเก็บเอาไว้ จำเป็นจะต้องหาผลตอบแทนที่ความเสี่ยงต่ำ ส่วนใหญ่กองทุนประกันสังคมจึงมักจะปล่อยกู้ให้กับรัฐบาลในรูปแบบของการซื้อพันธบัตร ประกันสังคมของสหรัฐเป็นเจ้าหนี้รายใหญ่ให้กับรัฐบาลมานาน ถือพันธบัตรสหรัฐอยู่เป็นสัดส่วนคือเกือบ 100% ของเงินกองทุน..!! ($2.7 ล้านล้าน) เป็นเจ้าหนี้อันดับ 1 ของรัฐบาล คิดเป็นสัดส่วนหนี้ประมาณ 14.4% ของมูลหนี้ $19 ล้านล้านเหรียญ มากกว่าปริมาณพันธบัตรสหรัฐที่ญี่ปุ่นกับจีนถือรวมกันเสียอีก..!!

แต่แนวโน้มอัตราดอกเบี้ยทั่วโลกที่ต่ำกว่าเงินเฟ้อ นั่นหมายความว่า เจ้าหนี้อย่างประกันสังคม ไม่เพียงแต่จะได้ผลตอบแทนต่ำลงเรื่อยๆ ยังจะเจอสถานการณ์ที่เงินต้นลดลงเมื่อเทียบกับเงินเฟ้อซะอีก และนี่เป็นระเบิดเวลาก้อนใหญ่ที่ซ่อนอยู่ในระบบประกันสังคมของประเทศพัฒนาแล้วแทบทุกประเทศ

รายได้น้อยลงฮวบฮาบ รายจ่ายเพิ่มขึ้นปรี้ดๆ แถมเงินกองกลางที่มีก็ผลตอบแทนต่ำติดดิน ถ้าปล่อยให้เป็นแบบนี้ต่อไป ระบบประกันสังคมของประเทศพัฒนาแล้วทั่วโลกก็จะเข้าสู่ภาวะล้มละลายในที่สุด (ประมาณการกันว่าระบบประกันสังคมของสหรัฐจะล้มละลายภายในไม่เกิน 10-20 ปีข้างหน้านี้แล้ว)

คำถามคือ ระบบประกันสังคมจะรอดได้ยังไง..?

a. หาทางเพิ่มรายได้..? อันนี้ยากมากถึงมากที่สุด ในเมื่อคนไม่มีงานทำ ประกันสังคมจะสร้างรายได้จากไหน

b. หาทางลดรายจ่าย..? อันนี้พอเป็นไปได้บ้าง ด้วยเทคโนโลยีที่พัฒนาอย่างก้าวกระโดด ต้นทุนการรักษาพยาบาลอาจจะลดลงเป็นเงาตามตัว แต่ก้างขวางคอชิ้นใหญ่คือ ธุรกิจยักษ์ใหญ่ในเซกเตอร์ healthcare แทบทั้งหมดไม่ใช่องค์กรการกุศล และคงจะไม่ช่วยรัฐในการลดต้นทุนได้ง่ายอย่างที่คิด

c. หาทางเพิ่มผลตอบแทนของกองทุน..? อันนี้จะมาพร้อมกับความเสี่ยง นั่นก็คือการที่กองทุนประกันสังคมจะทิ้งพันธบัตรรัฐบาล และโยกเงินไปลงทุนในสินทรัพย์อื่นที่ผลตอบแทนน่าจะสูงกว่า เช่น หุ้น หรือหุ้นกู้เอกชน

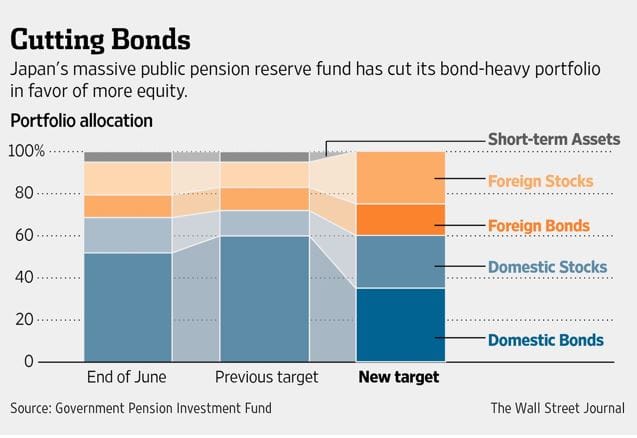

ตัวอย่างของทางออกนี้มีให้เห็นแล้วในปี 2014 กองทุนประกันสังคมของประเทศญี่ปุ่น (GPIF: Government Pension Investment Fund) ที่มีขนาดกองทุน $1.2 ล้านล้านเหรียญสหรัฐ ลดการถือพันธบัตรรัฐบาล และเพิ่มสัดส่วนการลงทุนในหุ้นญี่ปุ่นจาก 12% เป็น 25% หรือย้ายไปถือหุ้นถึง 1 ใน 4 ของกองทุน!! (และนี่เป็นเหตุผลหนึ่งที่ Nikkei วิ่งขึ้นมาเยอะมากในช่วง 2014-2015)

แต่แน่นอนว่าการตัดสินใจทางเลือกนี้ย่อม ‘เพิ่มความเสี่ยง’ ให้กับกองทุนอย่างเลี่ยงไม่ได้ ถ้าตลาดหุ้นพัง นั่นหมายถึงเงินของประชาชนจะหายไปทันที (Nikkei มี market cap ลดลงเกือบ 30% ในช่วงปลายปี 2015 ถึงกลางปี 2016 แน่นอนว่าเงินกองกลางของ GPIF ก็ลดลงตามไปด้วยไม่มากก็น้อย)

เราลองมาดูสมการกันว่า b = a + c ถ้าเกิด a ลดลงเร็วกว่า b ยังไงแล้วทางเลือกเดียวก็คือต้องเพิ่ม c ให้ได้

ในทางทฤษฏีถ้าจะเพิ่มผลตอบแทนของกองทุน มีแค่สองทางครับ ก็คือ ทิ้งพันธบัตร หรือเพิ่มผลตอบแทนให้พันธบัตรใหม่ ด้วยการขึ้นอัตราดอกเบี้ย หรืออาจจะต้องทำทั้งสองทาง

ความน่ากลัวของประกันสังคมของไทยคือ เราดันมีโครงสร้างประชากรแบบประเทศพัฒนาแล้ว (aging society) แต่ดันมีโครงสร้างเศรษฐกิจแบบประเทศกำลังพัฒนา นั่นแปลว่าในอนาคตเราจะมีคนวันชรามากขึ้นเต็มประเทศ โดยที่ส่วนใหญ่ยังจนอยู่ นั่นก็หมายถึงพวกเขาต้องพึ่งพาประกันสังคมมากขึ้น เพราะไม่มีเงินเก็บ ปัญหาของเราจึงมีแนวโน้มหนักกว่าประเทศพัฒนาแล้วมากๆ

Bloomberg เคยวิเคราะห์ไว้ว่า ประกันสังคมไทยมีโอกาสที่จะล้มละลายในอีกไม่เกิน 11 ปีหลังจากนี้ เตรียมใจกันไว้ซักนิดนะครับ ว่าประกันสังคมที่เราส่งเงินทุกเดือนอาจจะไม่เหลือเงินมาเลี้ยงดูเราตอนเราเกษียณ ปัญหานี้เป็นเรื่องที่ปวดหัวกันทั่วโลก ไม่ใช่แค่เมืองไทย

PS. ต้องบอกว่าการตัดสินใจของ GPIF ของญี่ปุ่นเป็นการตัดสินใจที่ถูกต้องหลังจากที่ตลาดหุ้นญี่ปุ่นทำ new all time high ในปี 2023 ที่ผ่านมา ทำให้สินทรัพย์ของกองทุน GPIF เพิ่มขึ้นแบบก้าวกระโดด ชดเชยกับผลตอบแทนพันธบัตรรัฐบาลญี่ปุ่นที่ต่ำเตี้ยเรี่ยดินมาหลายปี

In this post, I'd like to address the risks that social security funds (globally) may encounter in the future. This discussion aims to expand the understanding of individuals who are increasingly interested in the investment strategies of social security funds during this period. It's worth noting that this growing interest marks a positive trend, as previously, there was little to no attention paid to where social security funds invested their money, despite the fact that these funds essentially belong to us all.

To begin, it's essential to acknowledge that the challenges facing social security stem from aging societies.

The issue of aging societies has been a long-discussed topic. According to estimates from populationpyramid, it's projected that by 2100, Thailand's population will decrease from 68 million to around 40 million (-41%), while Japan's population will decline from 127 million to just 83 million (-34%).

In developed countries, the declining population is largely due to low birth rates among modern individuals who are less inclined to have children, as well as low mortality rates resulting from advances in medical technology. Conversely, in African countries, birth rates are increasing rapidly, leading to a significant shift in population structure across continents.

Now, let's consider a scenario where in developed countries, there's a shortage of job opportunities for the working-age population, leading to reduced government revenue from taxes. Additionally, social security systems would suffer significant losses in income.

Moreover, these countries would also face challenges related to the increasing number of retirees, compounded by job losses. While the government loses income, the number of retirees increases, creating a financial strain on social security systems.

Since 2010, the Social Security Trust Fund of the United States has been experiencing negative cash flow, with revenue collected from the working-age population falling short of the payments made to retirees, resulting in budget deficits. Projections indicate that the $2.7 trillion Social Security Trust Fund may be depleted, leaving nothing by the year 2030. Importantly, these estimates haven't factored in the accelerating pace of technological developments that could lead to increased unemployment among the working-age population in the next decade.

Another dilemma facing the social security funds of developed nations is the need for low-risk investment returns. Typically, social security funds allocate their reserves by lending to governments in the form of purchasing bonds. The Social Security Trust Fund of the United States, in particular, is a major creditor to the government, holding nearly 100% of its reserves in U.S. Treasury securities, amounting to approximately $2.7 trillion. This makes it the largest creditor to the U.S. government, accounting for around 14.4% of the $19 trillion national debt, surpassing the combined holdings of Treasury securities by Japan and China.

However, with global interest rates trending lower than inflation, social security creditors not only face diminishing returns but also risk erosion of principal when adjusted for inflation. This scenario poses a significant threat to the stability of social security systems in developed nations, with most countries facing similar challenges.

With declining revenues and escalating expenses, coupled with diminishing returns on investments, the social security systems of developed nations are on a collision course towards collapse. Without intervention, it's estimated that the social security system of the United States may face collapse within the next 10-20 years.

The question at hand is how social security systems can survive. Let's explore the potential avenues:

a. Increasing Revenue: This is perhaps the most challenging option, especially when the workforce is dwindling. Social security systems rely on contributions from the working-age population, but with unemployment rising, generating revenue becomes increasingly difficult.

b. Reducing Expenses: While challenging, technological advancements offer some hope in reducing healthcare costs. However, the dominant players in the healthcare sector are mostly profit-driven corporations, unlikely to aid in cost reduction efforts.

c. Enhancing Fund Returns: This option comes with increased risk. Social security funds could opt to reduce government bond holdings and allocate more resources to higher-yield assets like stocks or corporate bonds. A prime example of this approach is Japan's Government Pension Investment Fund (GPIF), which significantly decreased its government bond holdings and increased its exposure to Japanese equities from 12% to 25%. (And this is one reason why the Nikkei surged significantly during the period of 2014-2015.)

However, such decisions inevitably increase risk. If the stock market crashes, the immediate consequence is the loss of public funds. For instance, when the Nikkei index plummeted nearly 30% from late 2015 to mid-2016, the GPIF's assets declined accordingly.

It's a balancing act. If option a decreases faster than option b, the only recourse is to increase option c. In theory, there are only two ways to enhance fund returns: either by reducing bond holdings or increasing the returns on new bonds through higher interest rates. Practically, a combination of both approaches may be necessary.

The alarming aspect of Thailand's social security system is that we find ourselves in the demographic structure of a developed country (aging society) while maintaining an economy characteristic of a developing nation. This means that in the future, we will have a larger elderly population across the nation, with the majority still facing economic challenges. Consequently, they will increasingly rely on social security as they may not have sufficient savings. Our problem is thus more severe than that of developed countries.

Bloomberg has previously analyzed that Thailand's social security system could potentially collapse within the next 11 years. It's a warning we should take seriously, considering that the social security contributions we make monthly may not be sufficient to support us when we retire. This issue is a global concern, not exclusive to Thailand.

P.S. It must be noted that the decision made by Japan's Government Pension Investment Fund (GPIF) was a prudent one, especially after the Japanese stock market reached a new all-time high in 2023. This surge in the stock market significantly boosted the assets of the GPIF, compensating for the low returns from Japanese government bonds over several years.

Disclaimer: Avareum Research is an independent crypto research firm committed to providing unbiased and informative content. While we strive for complete objectivity, it's important to note that the research industry is inherently complex and may be influenced by various factors. To ensure transparency, we disclose any potential conflicts of interest, such as financial sponsorships or investments in the crypto space. Ultimately, all research and analysis provided by Avareum Research is intended for informational purposes only and should not be considered financial advice. Please consult with a qualified professional before making any investment decisions.

© 2024 Avareum Research. All Rights Reserved. This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.